First Home Buyer Loans | What’s Available to Help You Buy Your First Home

First Home Buyer Benefits Guide: What’s Available to Help You Buy Your First Home?

There’s never been more support available for first home buyers but navigating these benefits can be confusing. With this guide and the help of a Brisbane home loan broker, we explain the key perks and benefits to help you understand what’s available and how to make the most of them.

What is the First Home Guarantee (FHG)?

The First Home Guarantee (FHG) is a government scheme allowing eligible first home buyers and those re-entering the property market to buy an owner-occupied home with just a 5% deposit. Single parents may even qualify for a reduced 2% deposit.

For those re-entering the property market, eligibility requires that they have not owned property in the last 10 years.

Ordinarily, a deposit of less than 20% requires Lender’s Mortgage Insurance (LMI), which protects the lender and can cost tens of thousands of dollars. However, under the FHG, the government provides a guarantee that protects the lender, enabling you to avoid LMI. For example, on a $500,000 home, the lender would only require a $25,000 savings deposit. Keep in mind that additional fees, like stamp duty, may still apply—though first home buyers might qualify for a stamp duty concession (more on that below).

Deposit and Genuine Savings Requirements:

The deposit usually needs to consist of "genuine savings," meaning funds that have been in your account for at least three months to demonstrate consistent saving habits.

Some lenders may accept rental payment history as an alternative to genuine savings, which can be beneficial for buyers without long-standing savings.

Gifted funds may also be accepted as part of the deposit if they have been in your account for three months.

Other Key Criteria:

Property types: Eligible properties include newly built homes, established homes, and off-the-plan townhouses or apartments.

Income and price caps: These vary by location/post code.

Residency: You must be a citizen or permanent resident, and the property must remain owner-occupied during the guarantee period.

Loans under the First Home Guarantee must be with an approved lender, and must meet the eligibility criteria. It’s important to note that the government does not own a part of your property, and the guarantee can be released once you have 20% equity in your property. We recommend speaking with your broker if you think you might be eligible to release the guarantee.

Your property must also remain owner-occupied during the duration of the guarantee. If you wish to rent out your property, the guarantee must be released. This would require refinancing your loan, and you may need to pay Lender’s Mortgage Insurance (LMI) if there’s less than 20% equity in your property.

How Does the First Home Super Saver Scheme (FHSSS) Work?

The First Home Super Saver Scheme (FHSSS) is a government scheme that allows first home buyers trying to save their deposit to purchase a home to make voluntary additional super contributions, taxed at the applicable superannuation rate of 15%, rather than the applicant’s income tax bracket which is usually higher than 15%. This does not include the required minimum contribution your employer makes to your super, contributions must be additional to this.

First home buyers can contribute an additional $15,000 per financial year up to a total of $50,000 across multiple years. When they are ready to buy, they simply request their superannuation company release the funds. We recommend doing this as early as possible as it can take some time for the release request to be processed.

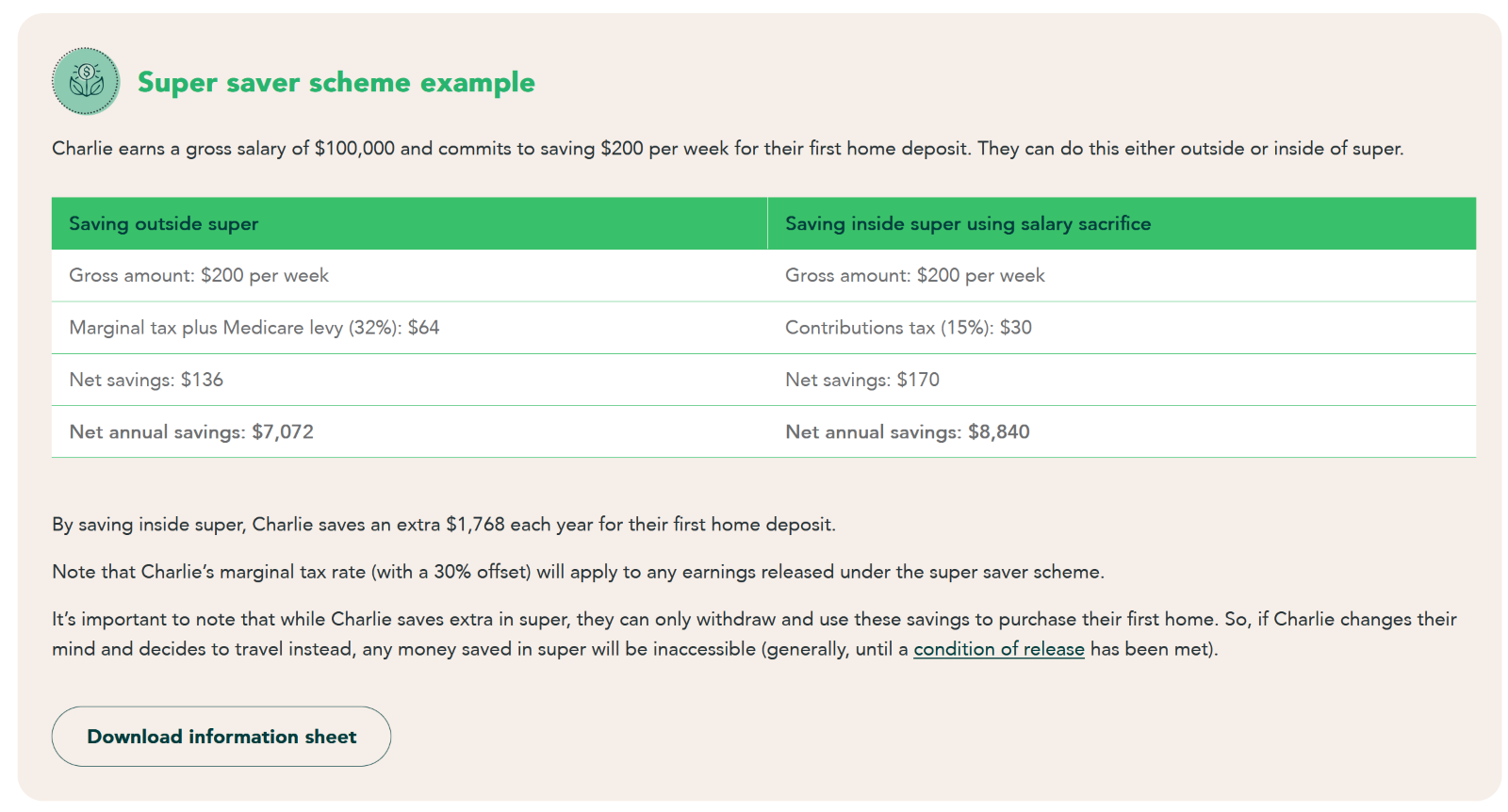

Check out this great example of how much can be saved from NGS Super:

Example savings calculations are referenced from NGS Super's First Home Super Saver Scheme Guide.

How much you can save is relevant to your taxable income and the contributions you’re making. We recommend speaking to an accountant to receive specific advice around your circumstances.

What is the First Home Owner’s Grant (FHOG)?

The First Home Owner’s Grant (FHOG) is a grant paid to first home buyers when purchasing a home. This can be between $10,000 and $30,000 depending on which state you are buying. It has specific requirements based on which state the property is being purchased in and is generally only available for new properties. This includes purchasing land and building a home or buying a new property off the plan like a townhouse or apartment.

There are several criteria, which often include:

- Income limits and property price caps (varies by state – refer to the specific state website for information).

- Occupancy requirements: Typically, you must occupy the property for a certain period.

The funds from the first home owner’s grant can form part of your deposit but usually only where applicants have a rental history with a real estate agent otherwise it will not likely form part of your minimum deposit but can be used towards your purchase. In most cases, the lender will apply for the grant on your behalf with your consent and funds will be paid directly to your lender.

Can I Get a Stamp Duty Concession?

Stamp duty is a tax levied by the state you are purchasing a property in. Each state has their own requirements and calculations as to what you will be required to pay and whether you can receive a reduction or concession. First home buyers in many states can pay $0 or a reduced amount should they live in the property for a set amount of time, usually 12 months.

This concession can add up to thousands of dollars saved and will help reduce the deposit required to purchase.

A conveyancer or solicitor in your relevant state can help provide specific advice as to what you are eligible for, and we recommend speaking to one before starting your property buying journey.

Can I Combine Multiple First Home Buyer Benefits?

Yes! Depending on your circumstances, you may combine several of these benefits for greater financial assistance.

Each of the above have their own resources available online with detailed information and eligibility quizzes to assist in determining what’s available to you.

We recommend booking in a time with one of our finance specialists at Hello Home Loans who can help determine your eligibility as well as calculate your borrowing power and deposit required.

Disclaimer: The information provided in this article is current as of 21st November 2024, and is intended as a general guide only. Benefits, eligibility criteria, and available schemes may change over time or vary by state/territory. We recommend consulting with a Hello Home Loans broker and visiting official government websites for the most up-to-date information specific to your circumstances before making any financial decisions.