What Does The Bank Look For When Assessing A Home Loan

Can You Get a Home Loan With a New Job, Casual Work or Self-Employment? Here's What Banks Really Look For

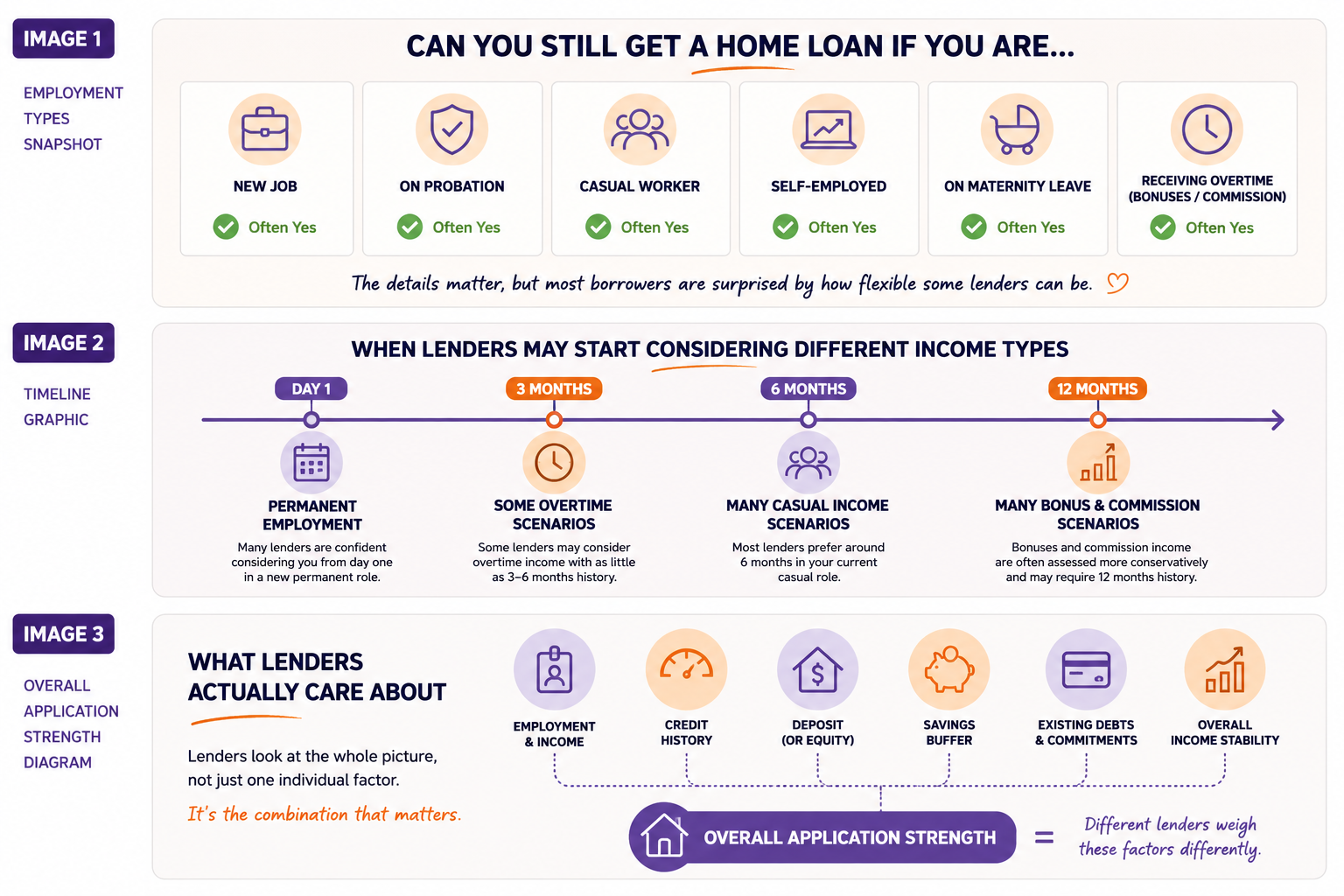

Jump to the section most relevant to you:

- Can You Get a Home Loan With a New Job?

- Can You Get a Home Loan While on Probation?

- Can You Get a Home Loan With Overtime, Bonuses or Commission Income?

- Can Self-Employed Borrowers Get a Home Loan?

- Common Employment Mistakes That Can Affect Your Home Loan Approval

- What Lenders Actually Care About

- Why Speaking To A Mortgage Broker Early Matters

- Frequently Asked Questions

One of the biggest misconceptions in lending is that changing jobs automatically stops you from getting a home loan.

In reality, it's far more nuanced than that.

A lot of people rule themselves out before they've even spoken to a mortgage broker because they assume:

- "I've only just started my new job"

- "I'm on probation"

- "I'm casual"

- "I changed industries"

- "I'm self-employed now"

…which means they think the bank will instantly decline them.

Sometimes that's true. Most of the time, it isn't.

What lenders actually care about is usually much broader than people realise. They look at:

- How stable your income is

- Whether there were long gaps between jobs

- Whether your income is ongoing

- What type of income you earn

- The overall strength of the application as a whole

That last part is important, because home loans are rarely assessed based on one single factor in isolation.

In our experience, a lot of borrowers get caught out because they're trying to figure out the answer themselves through Google, friends, TikTok or finance forums, when lending policy is often far more flexible and nuanced than people think.

And honestly, a lot of the real-world "rules" of lending aren't written down anywhere. They're things brokers learn over years of dealing with lenders, credit teams and different application scenarios.

Yes, you can often still get a home loan if you've recently changed jobs, you're on probation, you've returned from maternity leave, you're casual, or you've recently become self-employed.

But the details matter. For example:

- Changing jobs within the same industry is usually viewed more favourably

- Large gaps between employment can raise concerns

- Overtime, bonuses and commissions are treated differently from base salary

- Self-employed borrowers usually need more history than PAYG employees

- Some lenders are far more flexible than others

This is why two borrowers with the exact same income can sometimes get completely different outcomes depending on the lender chosen, how the application is structured, and whether the broker understands which lenders are likely to accept the scenario.

Can You Get a Home Loan With a New Job?

In many cases, yes.

One of the biggest myths in lending is that you need to be in your new job for six months or even twelve months before applying for a home loan. That's simply not true for a lot of borrowers.

If you're a PAYG employee earning a stable base salary, many lenders are perfectly comfortable considering your income from day one in a new role.

In fact, some lenders — including major banks like CBA and NAB — may even consider borrowers from day one of a new permanent role even if they were not working beforehand, provided the employment is ongoing and the rest of the application is strong.

What lenders are usually more interested in is whether there was a significant gap between jobs and whether the income is likely to continue.

For example, if someone moves from one full-time accounting role to another full-time accounting role with only a short gap in between, most lenders are not overly concerned.

Generally speaking:

- Gaps under one month are often fine

- Gaps under two months may still be acceptable with some lenders

- Gaps over three months may require stronger explanations or additional assessment

That doesn't automatically mean the loan will be declined. It simply means the lender may want more context around what happened during that period.

Can You Get a Home Loan While on Probation?

Yes, in many cases you can.

A lot of borrowers assume being on probation automatically means the bank will decline them, but that's often not the case at all.

In fact, many lenders are perfectly comfortable lending to borrowers from day one of a permanent full-time or permanent part-time role, even if they are still on probation.

Some major lenders may even consider borrowers who were previously unemployed before starting the role, provided the employment is ongoing and the overall application makes sense.

This surprises a lot of people because probation periods sound risky on paper, but in practice, probation by itself is often nowhere near as important as borrowers think it is.

This is one of the biggest misconceptions we see in lending. A lot of people rule themselves out before they even have a conversation because they assume: "I'm on probation, so I won't qualify."

Can You Get a Home Loan With Overtime, Bonuses or Commission Income?

This is where lending can start to become a bit more complicated.

A lot of borrowers assume: "I earn good money, so I'll qualify."

But lenders don't just look at how much you earn. They also look at how consistent and reliable that income is likely to be over time. That's why variable income is often assessed differently from standard base salary.

Overtime, bonuses and commissions are generally all assessed in a similar way by lenders. Unlike base salary, lenders usually want to see a history of this income before they will fully use it for borrowing capacity.

As a rough guide:

- Some lenders may consider overtime with as little as three to six months history

- Many lenders prefer around twelve months

- Bonuses and commission income are often assessed more conservatively again

At Hello Home Loans, we often jokingly refer to the 1st of October as "variable income day" — because that's when some lenders can finally start assessing the current financial year's overtime and extra income using the most recent three months rather than relying heavily on the previous financial year. That can become important if someone has recently started earning significantly more overtime or commission income but doesn't yet have enough current financial year history for the lender to use it.

Lender policy can also vary dramatically here. Two lenders may look at the exact same payslip and come up with completely different usable income figures. Some lenders annualise casual income over 48 weeks to account for assumed leave periods, while others may annualise it over the full 52 weeks if the income history already demonstrates consistency. The difference can have a surprisingly large impact on borrowing capacity.

Casual Employment

Casual employment is absolutely workable with many lenders, but most will want to see a history of stable income before considering it. In many cases:

- Six months in the current role is preferred

- Longer history is viewed more favourably

- Changing between casual jobs shortly before applying can make approval more difficult

Some allowances may also be usable immediately where they form part of an ongoing employment agreement and are clearly evidenced in the employment contract.

Can Self-Employed Borrowers Get a Home Loan?

Self-employed borrowers are often the most misunderstood when it comes to home loans.

A lot of business owners assume: "I make good money, so getting approved should be easy."

But lenders don't assess self-employed income the same way they assess PAYG employees. In many cases, mainstream lenders want to see at least one full year of financials before considering self-employed income, while some lenders may require even longer depending on the structure of the business and the overall application.

If there isn't enough history yet, borrowers may need to look at more specialist or second-tier lenders, which can sometimes come with higher interest rates.

How Tax Returns Affect Borrowing Capacity

One of the biggest issues we see is that many self-employed borrowers have never been properly educated on how their tax returns affect borrowing capacity.

Often, accountants are focused on minimising tax, while brokers are focused on maximising borrowing capacity — and those two goals do not always align.

For example, reducing taxable income may help minimise tax, but it can also significantly reduce the amount a lender is willing to approve. That's why communication between your broker and accountant can be incredibly important, especially leading into tax time if you are planning to buy property or refinance in the near future.

At Hello Home Loans, we are more than happy to work directly with accountants to help ensure the tax structure and lending strategy are aligned with the client's future plans.

This becomes even more important with company and trust structures, where income can often be more complex than a standard PAYG application. Different lenders assess self-employed income differently, treat add-backs differently and have very different levels of comfort depending on the structure and overall strength of the application.

Common Employment Mistakes That Can Affect Your Home Loan Approval

Changing Jobs During the Application Process

One of the biggest mistakes borrowers make is changing jobs during the application process without speaking to their broker first.

This becomes especially risky once a contract has been signed or the loan has already been formally approved.

A lot of borrowers assume that once formal approval has been issued, the deal is locked in and cannot change. That's not necessarily true.

If a lender becomes aware of a significant change to your financial circumstances before settlement, they are absolutely within their rights to reassess or even withdraw the approval — and yes, this does happen in the real world.

Unfortunately, borrowers can still be exposed to significant costs or penalties under the contract of sale even if the lender later pulls the approval before settlement. That's why major financial changes should never happen during the application process without first speaking to your broker.

For example, someone may move into a new role with similar overall pay, but if the application relied heavily on overtime, commissions or bonuses, changing jobs can reset that income history completely — significantly reducing borrowing capacity and, in some cases, completely changing the outcome of the application.

Assuming Salary Sacrifice or Car Leases "Don't Count"

This catches people out constantly. A lot of borrowers see deductions coming out of their payslip and assume: "That doesn't really affect me because it comes out before tax" or "It's only a lease, not a personal loan."

Unfortunately, lenders usually don't see it that way. Things like novated leases, salary sacrificed vehicles, employer-linked finance, and non-voluntary additional superannuation contributions can all significantly affect borrowing capacity.

This is especially common with government employees, where mandatory additional super contributions are often built into employment agreements and cannot simply be stopped to improve servicing.

In many cases, borrowers don't even mention these commitments because they don't think of them as debts — but they are often sitting clearly on the payslip for the lender to assess anyway, and sometimes the impact can be surprisingly large.

Temporary Higher Duties and Acting Roles

Another common misunderstanding happens when borrowers are temporarily earning a much higher income than normal — for example, in acting roles, higher duties allowances, temporary promotions, short-term contracts or temporary project-based income increases.

Borrowers can understandably become frustrated when lenders don't fully use that higher income. But from the lender's perspective, they are assessing whether the income is likely to continue long term. A bank may be writing a 30-year loan based on income that is only guaranteed for another six or twelve months.

That's why lenders are often more conservative with temporary income increases unless there is evidence the higher income is likely to continue permanently.

Government Payments and Other Non-Standard Income

Some lenders will accept payments such as Family Tax Benefit A and B, but usually only where the payments are expected to continue long term. Many lenders want to see that the benefit is likely to continue for at least another five years before fully considering it.

Other income types, such as workers compensation or permanent disability payments, can become more complex again. In many of those situations, borrowers may already be looking at more specialist lenders depending on the type of income, its long-term stability and the overall application.

Trying to Self-Assess Through Google

Honestly, this is one of the biggest mistakes we see. A lot of borrowers spend weeks convincing themselves they won't qualify because they've read a single lender policy online or spoken to one bank branch.

Different lenders assess income differently, calculate borrowing capacity differently, treat casual income differently, treat self-employed income differently, and have completely different appetites for risk.

That's why someone can be declined by one lender and approved comfortably by another. A lot of the real-world "rules" of lending are not written publicly anywhere — they're things brokers learn over years of dealing with credit teams, policy exceptions and lender behaviour.

Sometimes the difference between an approval and a decline simply comes down to lender choice, how the application is structured, and whether the broker understands how to present the scenario properly.

What Lenders Actually Care About

One of the biggest misconceptions in lending is that borrowers think there is usually one single reason they will or won't qualify.

In reality, lenders assess overall risk. That means a borrower with one weaker area in their application can still be approved very comfortably if the rest of the deal is strong. For example:

- Someone on probation may still be approved easily with strong savings and good credit

- A self-employed borrower may still qualify despite a more complex structure

- A borrower with a smaller deposit may still have strong servicing and stable financial conduct

- Someone with variable income may still qualify if there is enough history and consistency

A good broker is not just comparing interest rates. They are trying to understand which lender is most likely to suit the scenario, which income types are likely to be accepted, where policy exceptions may exist, and which parts of the application need to be strengthened before submission.

A lot of lender policy available publicly online is either oversimplified, outdated, missing context, or doesn't reflect how the lender behaves in practice.

Lender appetite also changes constantly. Sometimes banks actively want more of a certain type of lending. Other times they may quietly tighten policy or become far more conservative in particular areas — and often, borrowers would never know this was happening publicly.

That information is usually communicated internally to brokers, bankers and credit teams long before the average borrower notices anything has changed. Many of the most important parts of lending are never really written down publicly at all — they're the "unspoken rules" brokers learn over years of dealing with credit assessors, understanding lender behaviour, and recognising which scenarios are likely to work before the application is even submitted.

Why Speaking To A Mortgage Broker Early Matters

One of the biggest mistakes borrowers make is assuming they already know the answer before they've actually spoken to a mortgage broker.

A lot of people rule themselves out because they've recently changed jobs, they're on probation, they're self-employed, they've spoken to one bank, or they've read a lender policy online and assumed that applies everywhere.

But lending doesn't work that simply. Different lenders have completely different appetites for casual income, self-employed borrowers, high LVR lending, probationary employment, credit impairment, and variable income.

That's why someone can be declined by one lender and approved comfortably by another.

Broker experience varies significantly too. Some brokers are extremely experienced with complex lending scenarios, while others mainly deal with straightforward PAYG applications and may not know which lenders are more flexible in certain situations.

Sometimes a scenario genuinely isn't workable right now. But even then, a good broker should still be able to explain:

- What needs to improve

- How long you may need to wait

- Which parts of the application are causing problems

- What strategy may help strengthen the application moving forward

For example, maybe you only need another three months in your role. Maybe reducing a debt changes the outcome completely. Maybe a different lender is more suitable. Or maybe the deal simply needs to be structured differently.

That's why we always encourage borrowers not to self-reject too early. Even if the answer is "not yet," that's very different from "never." And sometimes borrowers are far closer to qualifying than they realise.

Frequently Asked Questions

Can I get a home loan with a new job?

Yes, in many cases you can. Many lenders are comfortable considering borrowers from day one of a new permanent full-time or part-time role, even if they are still on probation.

Can I get a home loan while on probation?

Often, yes. Being on probation does not automatically mean your application will be declined. Many lenders are comfortable with probationary employment, especially for permanent roles.

Can I get a home loan while on maternity leave or after returning to work?

Yes, in many cases you can. Once you return to work, lenders will often assess your income much like any other PAYG employee. Some lenders may also consider previous overtime, bonuses and commission income depending on your employment history and time away from work. Many lenders will also consider borrowers who are still on maternity leave, provided there is a clear return-to-work plan and sufficient evidence that repayments can be met until income resumes.

How long do I need to be employed before applying for a home loan?

There is no single rule that applies to every lender. Some lenders will consider permanent employees from day one in a role, while others may require longer employment history depending on the type of income and the overall application.

Can casual workers get home loans?

Absolutely. Most lenders simply want to see a stable history of casual income. In many cases, around six months in the current role is preferred, although policies vary significantly between lenders.

Do banks accept overtime, bonuses and commission income?

Yes, but lenders usually want to see a history of that income first. Some lenders may consider overtime with as little as three to six months history, while many prefer around twelve months. Bonuses and commission income are often assessed more conservatively.

Can I change jobs before settlement?

Potentially, but you should always speak to your broker first. Changing jobs during the application process can affect borrowing capacity and, in some cases, lenders can reassess or withdraw approval before settlement if there has been a significant change to your financial circumstances.

Can self-employed borrowers still get home loans?

Yes. Many mainstream lenders want to see at least one full year of financials, while newer businesses or more complex structures may require specialist lenders.

Do Family Tax Benefits count as income for a home loan?

Sometimes. Many lenders will consider Family Tax Benefit A and B if the payments are expected to continue long term — often for at least another five years.

Why did one lender decline me if another lender approved me?

Because lenders assess risk differently. Different lenders have different appetites for various income types, employment situations and borrower profiles. That's why lender choice can make such a significant difference.

Should I speak to a broker before changing jobs?

Always. Even a quick conversation beforehand can help identify whether changing jobs could affect your borrowing capacity, income assessment or loan approval.

Final Thoughts

One of the biggest misconceptions in lending is that borrowers think there is always one simple reason they will or won't qualify for a home loan.

In reality, lending is rarely that simple. Different lenders assess risk differently, policies change constantly, and many of the real-world "rules" of lending are never written down or found online.

That's why we always encourage borrowers not to rule themselves out too early. Whether you've recently changed jobs, you're on probation, you're self-employed, you're on maternity leave or you've simply been told "no" before — it's worth speaking to a mortgage broker before making assumptions.

Even if the answer is "not right now", a broker can give you a roadmap that ends with "Hello" to your new home. And sometimes, borrowers are far closer to qualifying than they realise.